|

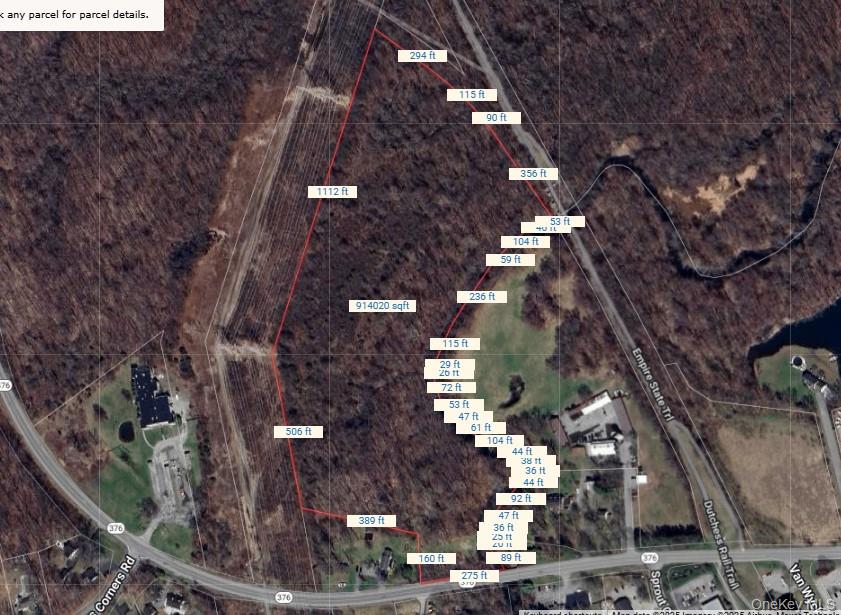

Lot 337829 Rt-376, Wappingers Falls, NY, 12590 | $99,000

Along the steady current of New York State Route 376 in Wappingers Falls, the parcel identified as Tax ID 0135689-6358-01-337829-0000 rests within the CC — Community Commercial — zone. It is land shaped as much by movement as by measurement. Route 376 is not a quiet back road. It is a connector — linking neighborhoods, schools, and nearby commercial hubs. Every day, traffic flows past in both directions, carrying potential customers, clients, and visibility. CC zoning recognizes that rhythm. It is written for corridors where business belongs, but where structure and planning matter just as much as exposure. Community Commercial zoning invites retail storefronts, professional offices, medical space, restaurants, and service-oriented businesses. It requires thoughtful site planning — parking calculated to the use, setbacks that create order, landscaping that softens edges, and review that ensures compatibility with surrounding properties. It is commerce with guardrails. Standing at the edge of the parcel, you can imagine the transformation. A well-designed building facing the road. Clean signage visible to passing drivers. Organized ingress and egress that respect the highway. The kind of commercial presence that serves the community rather than overwhelms it. What makes this property compelling is alignment. The zoning matches the corridor. The corridor carries demand. The surrounding rooftops generate daily need — for services, food, professional space, convenience. In commercial real estate, that alignment reduces risk and sharpens vision. This isn’t speculative land waiting for a variance or a change in code. The framework is already in place. The CC designation sets the boundaries and opens the door at the same time. It defines what belongs here and, just as importantly, what does not. On Route 376, opportunity moves with traffic. This parcel sits in that current — positioned, visible, and ready for a concept that understands how location and zoning work together to create lasting value. ****5 OTHYER LOTS AVAILABLE AS SHOWN IN PICTURES****

Features

- Elem. School: Myers Corners

- Middle School: Van Wyck Junior High School

- High School: Roy C Ketcham Senior High Sch

- School District: Wappingers

- MLS#: 963904

- Days on Market: 139 days

- Website: https://www.raveis.com

/prop/963904/lot337829rt376_wappingersfalls_ny?source=qrflyer

William Raveis Family of Services

Our family of companies partner in delivering quality services in a one-stop-shopping environment. Together, we integrate the most comprehensive real estate, mortgage and insurance services available to fulfill your specific real estate needs.

Customer Service

888.699.8876

Contact@raveis.com

Our family of companies offer our clients a new level of full-service real estate. We shall:

- Market your home to realize a quick sale at the best possible price

- Place up to 20+ photos of your home on our website, raveis.com

- Provide frequent communication and tracking reports showing the Internet views your home received on raveis.com

- Showcase your home on raveis.com with a larger and more prominent format

- Give you the full resources and strength of William Raveis Real Estate, Mortgage & Insurance and our cutting-edge technology

To learn more about our credentials, visit raveis.com today.

Frank KolbSenior Vice President - Coaching & Strategic, William Raveis Mortgage, LLC

NMLS Mortgage Loan Originator ID 81725

203.980.8025

Frank.Kolb@raveis.com

Our Executive Mortgage Banker:

- Is available to meet with you in our office, your home or office, evenings or weekends

- Offers you pre-approval in minutes!

- Provides a guaranteed closing date that meets your needs

- Has access to hundreds of loan programs, all at competitive rates

- Is in constant contact with a full processing, underwriting, and closing staff to ensure an efficient transaction

Lot 337829 Rt-376, Wappingers Falls, NY, 12590

$99,000

Customer Service

William Raveis Real Estate

Phone: 888.699.8876

Contact@raveis.com

Frank Kolb

Senior Vice President - Coaching & Strategic

William Raveis Mortgage, LLC

Phone: 203.980.8025

Frank.Kolb@raveis.com

NMLS Mortgage Loan Originator ID 81725

|

5/6 (30 Yr) Adjustable Rate Conforming* |

30 Year Fixed-Rate Conforming |

15 Year Fixed-Rate Conforming |

|

|---|---|---|---|

| Loan Amount | $79,200 | $79,200 | $79,200 |

| Term | 360 months | 360 months | 180 months |

| Initial Interest Rate** | 6.125% | 6.500% | 5.750% |

| Interest Rate based on Index + Margin | 8.125% | ||

| Annual Percentage Rate | 6.424% | 6.650% | 5.972% |

| Monthly Tax Payment | N/A | N/A | N/A |

| H/O Insurance Payment | $75 | $75 | $75 |

| Initial Principal & Interest Pmt | $481 | $501 | $658 |

| Total Monthly Payment | $556 | $576 | $733 |

* The Initial Interest Rate and Initial Principal & Interest Payment are fixed for the first and adjust every six months thereafter for the remainder of the loan term. The Interest Rate and annual percentage rate may increase after consummation. The Index for this product is the SOFR. The margin for this adjustable rate mortgage may vary with your unique credit history, and terms of your loan.

** Mortgage Rates are subject to change, loan amount and product restrictions and may not be available for your specific transaction at commitment or closing. Rates, and the margin for adjustable rate mortgages [if applicable], are subject to change without prior notice.

The rates and Annual Percentage Rate (APR) cited above may be only samples for the purpose of calculating payments and are based upon the following assumptions: minimum credit score of 740, 20% down payment (e.g. $20,000 down on a $100,000 purchase price), $1,950 in finance charges, and 30 days prepaid interest, 1 point, 30 day rate lock. The rates and APR will vary depending upon your unique credit history and the terms of your loan, e.g. the actual down payment percentages, points and fees for your transaction. Property taxes and homeowner's insurance are estimates and subject to change.

William Raveis Mortgage, LLC, NMLS ID 2630, 7 Trap Falls Road, Shelton, CT 06484

NY Licensed Mortgage Banker-NYS Banking Department LMBC 106535